You'll have to visit the Sad Guys On Trading Floors website and read the captions to truly appreciate the pictures.

![[Insert “Bear Market” joke here]](http://5.media.tumblr.com/bLjlTcuJUr33tded4nZeOGBCo1_400.jpg)

"A Cabarrus County man swindled $30 million from investors and spent it on lavish cars, expensive artwork and a 45-acre horse farm, former investors charge in a pair of lawsuits filed in Mecklenburg court recently."

"The scheme involved 60 investors and spanned four years, ending after the man, Bruce Kramer, committed suicide, prompting investors to check the status of their money, court documents say."

"“It's a sad time for a lot of families,” said John Manzella of Charlotte, an investor named in one of the suits. “This has hurt a lot of people, financially as well as emotionally.”"

![[Stocks Surge]](http://s.wsj.net/public/resources/images/OB-DG818_0310st_D_20090310160756.jpg)

"There were far more failures here than I expected. I've been chagrined at how badly some of the judgments of very sophisticated investors have been with respect to risks...It's all human psychology with which we're dealing, not institutions. The argument, therefore, is not to discard counterparty surveillance, but, essentially, to patch it back together."

"In carrying out this scheme, the SEC claims, Messrs. Stanford and Davis misappropriated billions of investors' money and falsified the Stanford International Bank's records to hide their fraud.

"Stanford International Bank's financial statements, including its investment income, are fictional," the SEC said."

Stanford Accused of a Long-Running Scheme

ProbabilitySpecifically, this is a joint default probability—the likelihood that any two members of the pool (A and B) will both default. It's what investors are looking for, and the rest of the formula provides the answer. | Survival timesThe amount of time between now and when A and B can be expected to default. Li took the idea from a concept in actuarial science that charts what happens to someone's life expectancy when their spouse dies. | EqualityA dangerously precise concept, since it leaves no room for error. Clean equations help both quants and their managers forget that the real world contains a surprising amount of uncertainty, fuzziness, and precariousness. |

CopulaThis couples (hence the Latinate term copula) the individual probabilities associated with A and B to come up with a single number. Errors here massively increase the risk of the whole equation blowing up. | Distribution functionsThe probabilities of how long A and B are likely to survive. Since these are not certainties, they can be dangerous: Small miscalculations may leave you facing much more risk than the formula indicates. | GammaThe all-powerful correlation parameter, which reduces correlation to a single constant—something that should be highly improbable, if not impossible. This is the magic number that made Li's copula function irresistible. |

"Low worldwide interest rates and credit spreads have let to strong client demand for credit instruments, and the growth in notional volumes reflects that," said Dick. "Our large dealer banks have targeted credit derivatives as an important segment of their product mix, and a critical aspect of our supervision is to work with other agencies to ensure that the dealer community has the appropriate operational infrastructure to support this growing market".

Risky Business: Credit Derivatives (pdf )8/18/05, The Economist

"Of course, things can go wrong. It is possible that the pricing of ever more complicated instruments might sometimes be too much even for the ultra-brainy lot who do it, with expensive results. Tranched instruments have no clear market price, so they have to be valued with complex models. Working out whether a default in a portfolio is likely to be an isolated event, or is a harbinger of more to come, is especially tricky, not least because data on credit defaults are relatively sparse. Some worry about the increased activity of hedge funds which, lured by the yield on illiquid, complicated instruments, make up as much as 70% of trading volume in credit derivatives, by some counts."

"In a special two-hour report, CNBC's David Faber takes an in-depth look at the causes of the ongoing collapse of the housing industry."

* Saturday, February 14, 2009 at 7p/10p ET

* Sunday, February 15, 2009 at 9p ET

* Monday, February 16, 2009 at 6a/8p/12a ET

* Saturday, March 1, 2009 at 12a ET

* Sunday, March 15, 2009 at 9p ET

Watch CNBC's House of Cards Thursday Night

"Faber follows the story from mortgage broker to homeowner, brokers to ratings agencies and all the way to former Federal Reserve Chairman Alan Greenspan. Most of what preceded the credit meltdown, which started in September 2007, happened under his watch, and in Faber’s interview, Greenspan admits that even he couldn’t explain collateralized debt obligations – and he had a couple of hundred Ph.D.s on staff." -Tom Brennan, CNBC

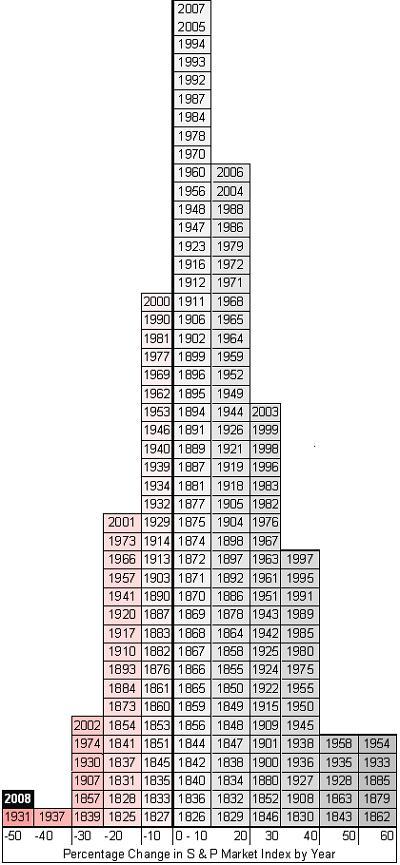

"On this chart each block represents a year and each column represents a range of return on the S&P index. Over on the right side are those lucky years where the index has soared upward from 50-60%. In the middle are the more typical years, where the market has risen less than 10%. That little box on the far left? Yeah, that's this year..And hey, how many of you knew the S&P had been around since 1825?." - Devilstower of the Daily KOS

{kind=link}